30-year mortgage refinance rates hit highest point since July: Time to refinance? | Sept. 29, 2021

Our goal here at Credible Operations, Inc., NMLS Number 1681276, referred to as "Credible" below, is to give you the tools and confidence you need to improve your finances. Although we do promote products from our partner lenders, all opinions are our own.

Check out the mortgage refinancing rates for Sept. 29, 2021, which are up from yesterday for two key terms.

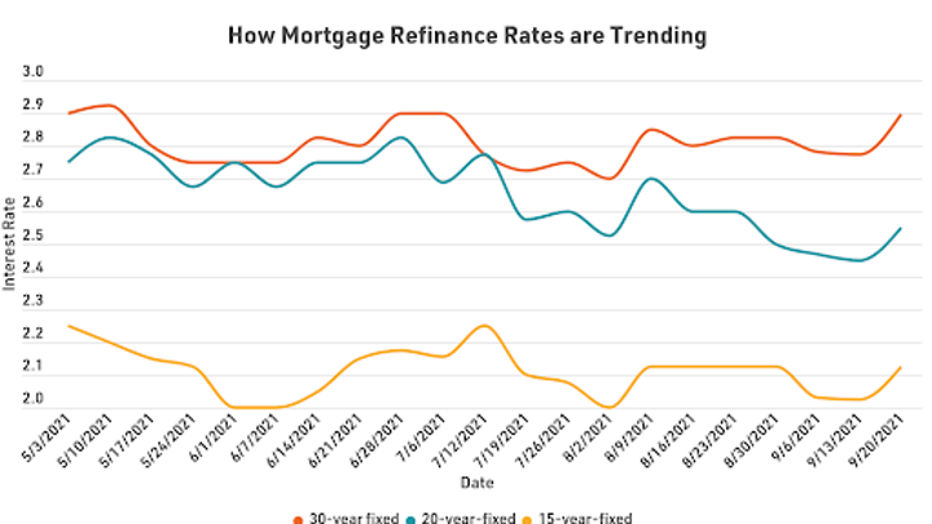

Based on data compiled by Credible, current mortgage refinance rates rose for 30-year and 10-year terms, while holding steady for 20-year and 15-year terms. At 3%, 30-year mortgage refinance rates are the highest they’ve been since July 2, 2021.

- 30-year fixed-rate refinance: 3.000%, up from 2.875%, +0.125

- 20-year fixed-rate refinance: 2.750%, unchanged

- 15-year fixed-rate refinance: 2.250%, unchanged

- 10-year fixed-rate refinance: 2.250%, up from 2.125%, +0.125

Rates last updated on Sept. 29, 2021. These rates are based on the assumptions shown here. Actual rates may vary.

Despite today’s increases, refinance rates remain near historic lows. Even after edging up to 3% today, 30-year rates are well below the year’s high of 3.375%, which occurred on Feb. 26. And 15-year refinance rates, which have held at or below 2.250% for 53 days, may be particularly appealing to homeowners looking to shorten their repayment term and secure a reliably low interest rate.

If you’re thinking of refinancing your home mortgage, consider using Credible. Whether you're interested in saving money on your monthly mortgage payments or considering a cash-out refinance, Credible's free online tool will let you compare rates from multiple mortgage lenders. You can see prequalified rates in as little as three minutes.

Current 30-year fixed refinance rates

The current rate for a 30-year fixed-rate refinance is 3.000%. This is up from yesterday. Refinancing a 30-year mortgage into a new 30-year mortgage could lower your interest rate, but may not have much effect on your total interest costs or monthly payment. Refinancing a shorter term mortgage into a 30-year refinance could result in a lower monthly payment but higher total interest costs.

Current 20-year fixed refinance rates

The current rate for a 20-year fixed-rate refinance is 2.750%. This is the same as yesterday. By refinancing a 30-year loan into a 20-year refinance, you could secure a lower interest rate and reduced total interest costs over the life of your mortgage. But you may get a higher monthly payment.

Current 15-year fixed refinance rates

The current rate for a 15-year fixed-rate refinance is 2.250%. This is the same as yesterday. A 15-year refinance could be a good choice for homeowners looking to strike a balance between lowering interest costs and retaining a manageable monthly payment.

Current 10-year fixed refinance rates

The current rate for a 10-year fixed-rate refinance is 2.250%. This is up from yesterday. A 10-year refinance will help you pay off your mortgage sooner and maximize your interest savings. But you could also end up with a bigger monthly mortgage payment.

You can explore your mortgage refinance options in minutes by visiting Credible to compare rates and lenders. Check out Credible and get prequalified today.

Rates last updated on Sept. 29, 2021. These rates are based on the assumptions shown here. Actual rates may vary.

These rates are based on the assumptions shown here. Actual rates may vary.

If you think refinancing is the right move, consider using Credible. You can use Credible's free online tool to easily compare multiple mortgage refinance lenders and see prequalified rates in as little as three minutes.

Rates last updated on Sept. 29, 2021. These rates are based on the assumptions shown here. Actual rates may vary.

The factors behind today’s refinance rates

Current refinance rates, like mortgage interest rates in general, are affected by many economic factors, like unemployment numbers and inflation. But your personal financial history will also determine the rates you’re offered when refinancing your mortgage.

Larger economic factors

- Strength of the economy

- Inflation rates

- Employment

- Consumer spending

- Housing construction and other market conditions

- Stock and bond markets

- 10-year Treasury yields

- Federal Reserve policies

Personal economic factors

- Credit score

- Credit history

- Home equity

- Loan amount, loan term, and loan type

- Debt-to-income ratio

- Location of the property

How to get your lowest mortgage refinance rate

If you’re interested in refinancing your mortgage, improving your credit score and paying down any other debt could secure you a lower rate. It’s also a good idea to compare rates from different lenders if you're hoping to refinance so you can find the best rate for your situation.

Borrowers can save $1,500 on average over the life of their loan by shopping for just one additional rate quote, and an average of $3,000 by comparing five rate quotes, according to research from Freddie Mac.

Be sure to shop around and compare rates from multiple mortgage lenders if you decide to refinance your mortgage. You can do this easily with Credible’s free online tool and see your prequalified rates in only three minutes.

How does Credible calculate refinance rates?

Changing economic conditions, central bank policy decisions, investor sentiment and other factors influence the movement of mortgage refinance rates. Credible average mortgage refinance rates are calculated based on information provided by partner lenders who pay compensation to Credible.

The rates assume a borrower has a 740 credit score and is borrowing a conventional loan for a single-family home that will be their primary residence. The rates also assume no (or very low) discount points and a down payment of 20%.

Credible mortgage refinance rates will only give you an idea of current average rates. The rate you receive can vary based on a number of factors.

Are refinance rates higher than purchase rates?

Refinance rates are generally higher than rates for new mortgages to buy a house. Here are some factors that influence the higher rates:

- Risk — A borrower who refinances into a shorter term to get a lower interest rate and pay off their loan sooner may end up with a higher monthly payment. That higher payment could translate into an elevated risk of default. Likewise, in cash-out refinances, the borrower’s debt-to-income ratio rises — and possibly their risk of defaulting.

- Revenue — A lender may be able to make more money off a purchase loan than a refinance. Many homebuyers choose longer terms for purchase mortgages, which come with higher interest rates. Refinancing into a shorter term and/or lower interest rate reduces the amount of interest the lender makes over the life of a loan.

- Costs — Refinancing a mortgage comes with many of the same closing costs you’ll face when you take out a new mortgage, such as an appraisal, attorney fees and more. Closing on a refinance also has costs for the lender. But whereas the lower interest rate and shorter term you get with a refinance benefits you financially, the lender will make less in interest over the life of the refinanced loan.

- Your credit — Hopefully, your credit continues to improve once you become a homeowner. But that’s not always the case for everyone. A homeowner whose credit score has actually fallen since they initially bought the house may look like a bigger risk to lenders — who may charge a higher interest rate to offset the perceived risk.

Credible is also partnered with a home insurance broker. If you're looking for a better rate on home insurance and are considering switching providers, consider using an online broker. You can compare quotes from top-rated insurance carriers in your area — it's fast, easy and the whole process can be completed entirely online.

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.

As a Credible authority on mortgages and personal finance, Chris Jennings has covered topics that include mortgage loans, mortgage refinancing, and more. He’s been an editor and editorial assistant in the online personal finance space for four years. His work has been featured by MSN, AOL, Yahoo Finance, and more.